Original title: Bitcoin - the trade after the trade

Original author: fejau

Original translation: TechFlow

I want to write down a question I have been thinking about for a long time: how Bitcoin might behave in the event of a major shift in capital flows, a situation that Bitcoin has never experienced since its inception.

I think Bitcoin will usher in an incredible trading opportunity once deleveraging is over. In this article, I will elaborate on my thoughts in detail.

What are the historical key drivers of Bitcoin price?

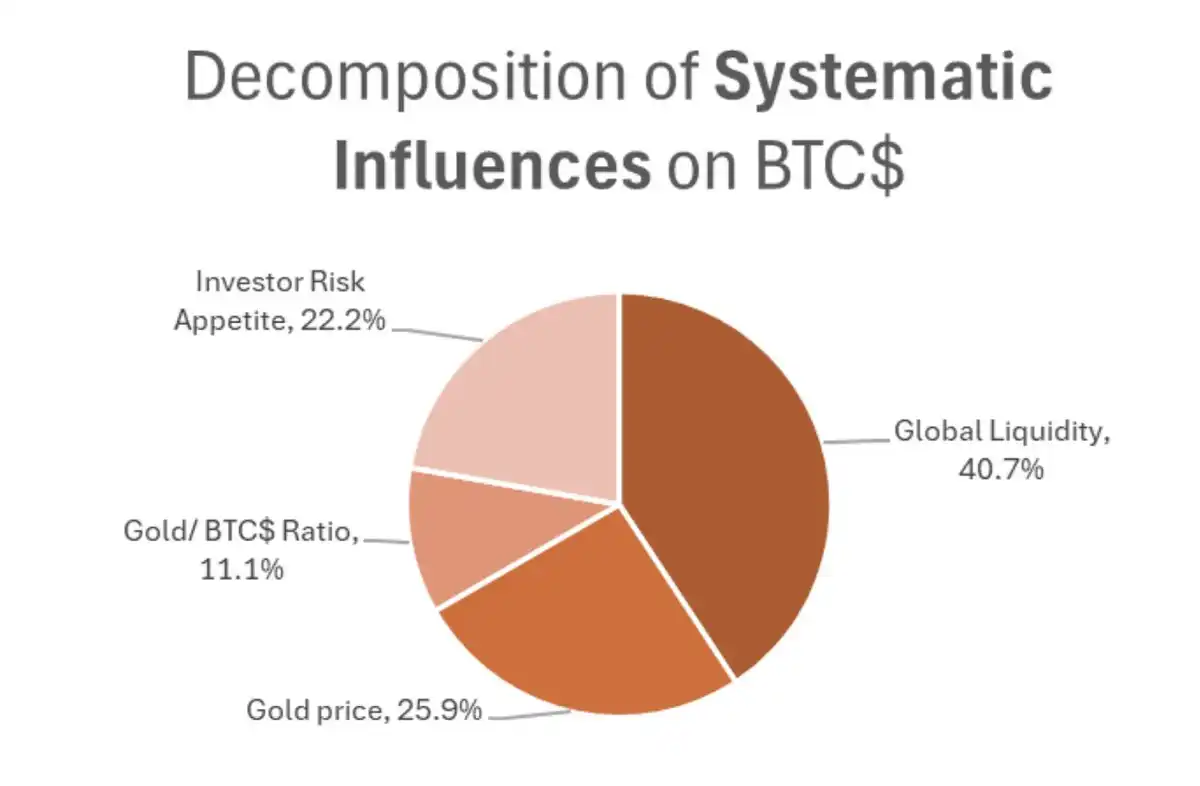

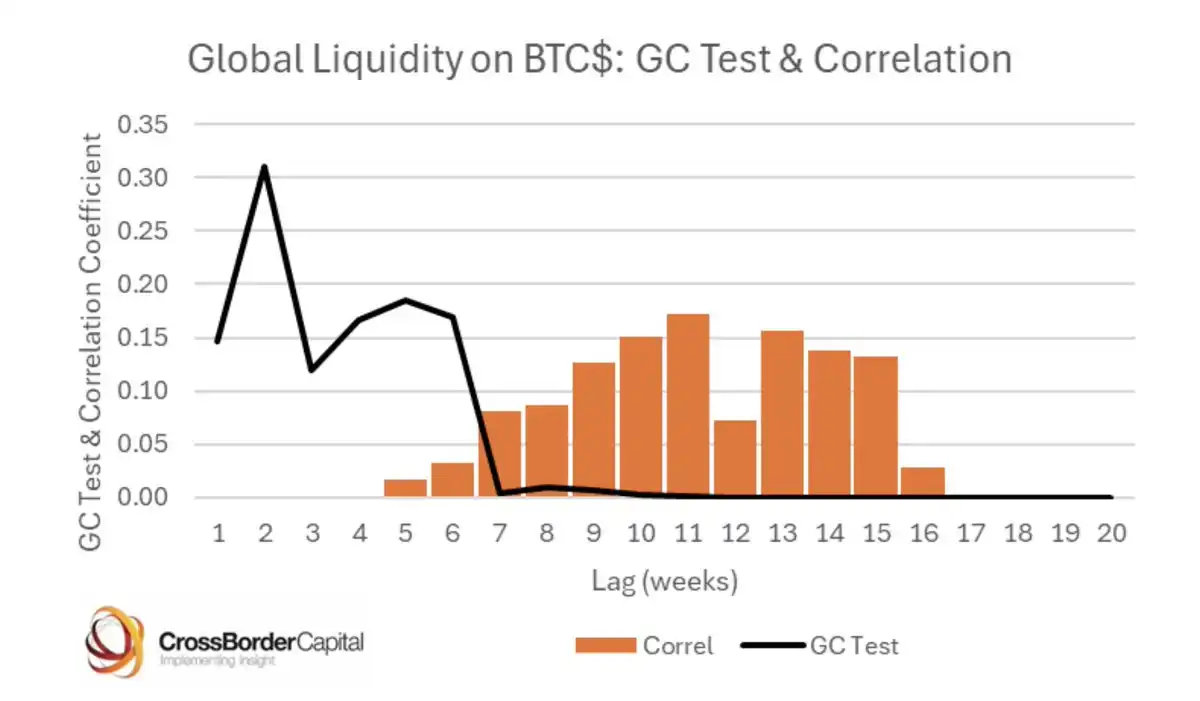

I will take Michael Howell’s research on historical drivers of Bitcoin’s price and use these to further understand how these crossover factors may evolve in the near future.

As shown in the above image, the drivers of Bitcoin include:

· Overall demand for high-risk, high-beta assets from investors

Relevance to gold

· Global liquidity

Since 2021, I have used a simple framework to understand risk appetite, gold performance and global liquidity, i.e. focusing on fiscal deficits as a percentage of GDP as an easy way to understand the fiscal stimulus that has dominated global markets since 2021.

Higher fiscal deficits as a percentage of GDP mechanically lead to higher inflation, higher nominal GDP, and therefore the total revenue of the firm is also higher, as income is a nominal indicator. This is a boon for companies that can enjoy economies of scale.

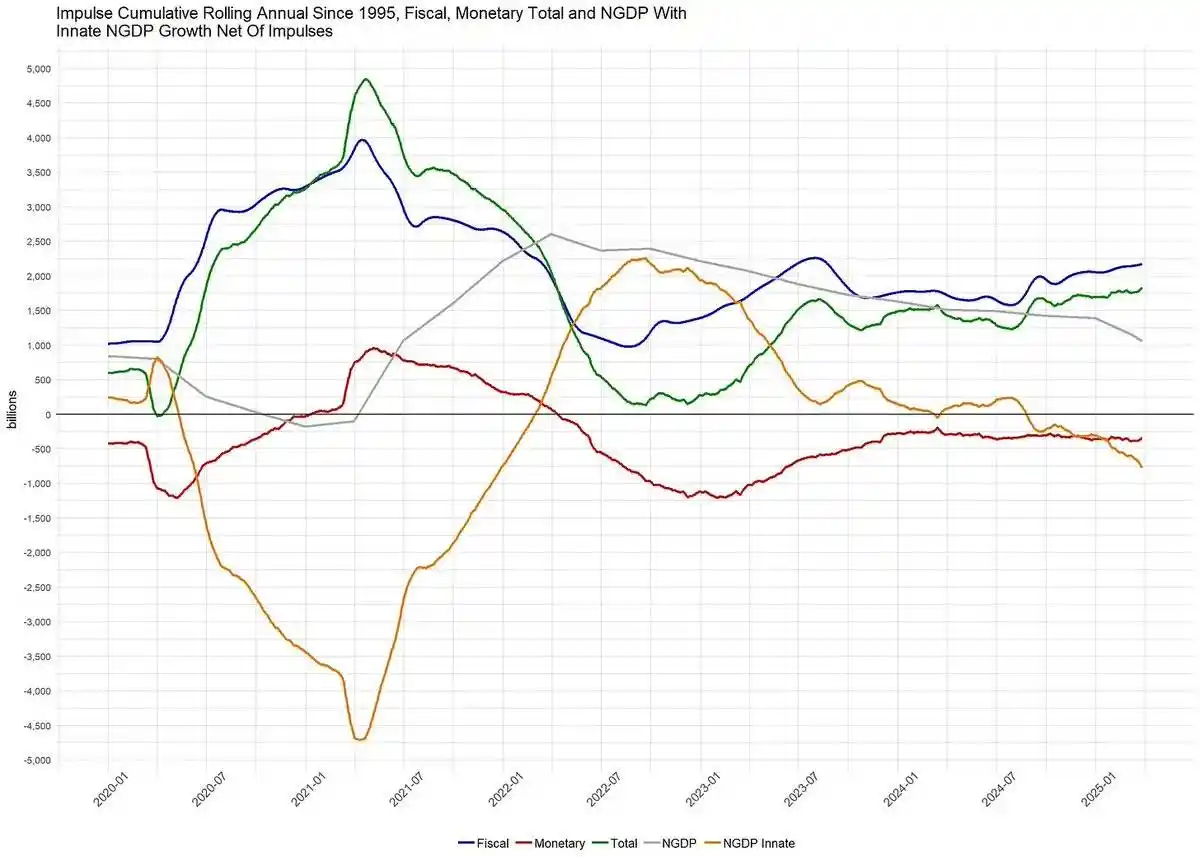

In most cases, monetary policy plays a secondary role in risk asset activities, and fiscal stimulus has been the main driver. As shown in this chart regularly updated by @BickerinBrattle, the monetary stimulus in the United States is so weak compared to fiscal stimulus that I put it aside in this discussion.

As shown in the chart below, the U.S. fiscal deficit accounts for a much higher proportion of GDP among the major developed Western economies than any other country.

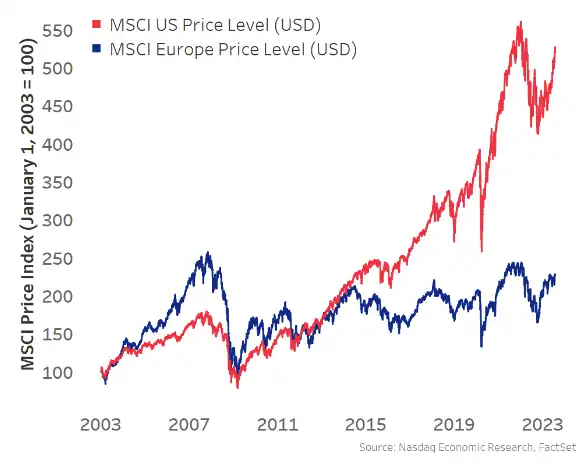

Due to such a large deficit in the U.S., revenue growth has been dominant and has led to outstanding performance in the U.S. stock market compared to other modern economies:

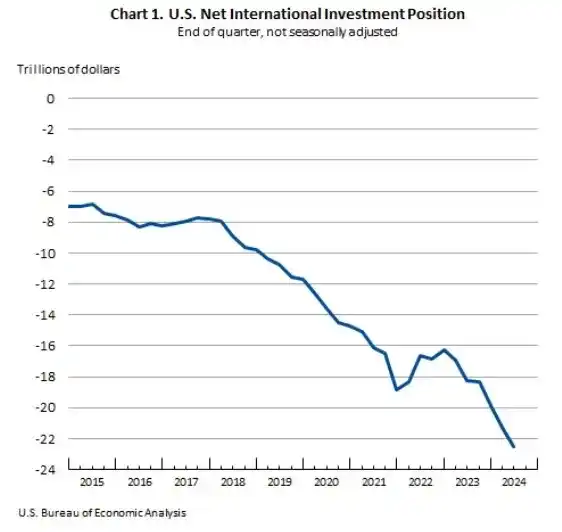

Due to this dynamic, the US stock market has become the main marginal driver of risk asset growth, wealth effect, and global liquidity, and therefore has become an attraction for global capital: the United States. The U.S. has become the main driver of global risk appetite due to the dynamic of capital flowing into the U.S., coupled with a huge trade deficit, which are traded in goods for foreign-obtained dollars, which are then reinvested in U.S. dollars denominated in U.S. dollars (such as Treasury bonds and MAG7).

Now, back to Michael Howell's research above. Risk preference and global liquidity have been driven primarily by the United States over the past decade, and this trend has accelerated since the COVID-19 pandemic due to such a huge fiscal deficit in the United States operating compared to other countries.

Therefore, Bitcoin, despite being a global liquid asset (not just the United States), has become increasingly positively correlated with U.S. stock markets since 2021.

Now, I think the correlation with the U.S. stock market is false. When I use the word "false correlation" here, I start from a statistical point of view and think that the third dependent variable that is not shown in the correlation analysis is the actual driving factor. I believe this factor is global liquidity, which, as we mentioned above, has been dominated by the United States for nearly a decade.

As we dig into statistical significance, we must also establish causality, not just positive correlations. Fortunately, Michael Howell has also done some great work in this regard, establishing a causal relationship between global liquidity and Bitcoin through the Granger causality test.

So, what kind of benchmark starting point does this provide us?

Bitcoin is driven primarily by global liquidity, and false correlations emerge as the United States is the main driver of the increase in global liquidity.

Over the past month, some major narratives have surfaced as we speculate about Trump’s trade policy goals and global restructuring of capital and commodity flows. I think of it as:

The Trump administration wants to reduce its trade deficit with other countries, which mechanically means reducing the flow of dollars to foreign countries, which will not be reinvested in U.S. assets. A reduction in the trade deficit cannot occur without this happening.

The Trump administration believes that foreign currencies are artificially suppressed, so the dollar is artificially strong and hopes to rebalance this. In short, weaker USD and stronger foreign currencies will cause interest rates to rise in other countries, prompting capital backflows to capture these rates that perform better under foreign exchange-adjusted conditions, as well as domestic stocks.

Trump’s “fire shots first, ask questions” approach in trade negotiations has led the rest of the world to get rid of a meager fiscal deficit compared to the United States (as mentioned above) and instead invest in defense, infrastructure and general protectionist government investments to make it more self-sufficient. Regardless of whether the tariff negotiations are downgraded (such as China), I believe this is a foregone conclusion and countries will continue to pursue this goal.

Trump hopes other countries will increase their defense spending as a percentage of GDP and contribute more to NATO spending, as the United States bears a lot of expenses in this regard. This will also increase the fiscal deficit.

I will put my personal views on these views for the time being and focus on the impact they may have if we advance according to the logical endpoints of these narratives:

Capital will leave assets denominated in US dollars and return to its home country. This means that U.S. stock markets perform poorly relative to the rest of the world, bond yields rise and the dollar weakens.

This capital will flow back to places where fiscal deficits are no longer limited, and other modern economies will start spending and printing money to fund these increased deficits.

As the United States moves from a global capital partner to a more protectionist role, those holding dollar assets will have to increase the risk premium of these once perfect assets and label them a broader margin of security. As this process progresses, it will lead to higher bond yields, and foreign central banks will seek to diversify their balance sheets, get rid of mere U.S. Treasuries and turn to other neutral commodities such as gold. Similarly, foreign sovereign wealth funds and pensions may pursue this diversity.

The opposite of these views is that the United States is the center of innovation and technology-driven growth, and no country will overturn this idea. Europe is too bureaucratic and socialist to pursue capitalism like the United States. I sympathize with this view, which may mean that this is not a multi-year trend, but a medium-term trend, as the valuations of these tech companies will limit their upside space for some time.

Going back to the title of this post, the first deal is to sell too many dollar assets held by the world to avoid ongoing deleveraging. Because the world holds too much of these assets, this deleveraging can become confusing when risk limits are touched by more speculative players such as large capital managers and multi-strategy hedge funds with strict stop loss. When this happens, we see days like margin additions where all assets need to be sold to raise cash. Now, the strategy for trading is to survive and keep it well-funded.

However, as deleveraging subsides, the next step of trading begins – shifting to a more diversified portfolio: foreign stocks, foreign bonds, gold, commodities, and even Bitcoin.

We have begun to see this dynamic forming in the market rotation day and non-margin day. The US dollar index (DXY) fell, U.S. stocks performed worse than stock markets in other regions, gold soared, and Bitcoin was unexpectedly strong compared to traditional U.S. technology stocks.

I believe that as this happens, the marginal increase in global liquidity will turn to the exact opposite dynamics we are used to. Other regions will assume the responsibility of increasing global liquidity and risk appetite.

As I ponder the risks of this diversification in the context of the global trade war, I worry too deeply into the tail risk of risky assets in other countries, as there are some big mines in terms of potentially bad tariff news. Therefore, this makes gold and Bitcoin the choice for global diversification in this transition.

Gold has been rising absolutely and is now setting new all-time highs every day, reflecting this institutional change. However, while Bitcoin has been surprisingly strong throughout the institutional shift, its correlation with risk appetite has so far limited its performance and failed to keep up with gold's performance.

So as we move towards a global capital rebalancing, I believe the transaction after this is Bitcoin.

When I compare this framework with Howell's relevance studies, I can see them combined:

The U.S. stock market cannot be affected by global liquidity, but only by liquidity measured by fiscal stimulus plus some capital inflows (but we just confirmed that aspect of this flow may stop or even reverse). However, Bitcoin is a global asset, reflecting a broad perspective of this global liquidity.

As this narrative is established and the risk allocators continue to rebalance, I believe risk preferences will be driven by other regions rather than the United States.

Gold performs very well, so we can also check it out here for the bitcoin section related to gold.

Given all this, I have seen for the first time in the financial market that Bitcoin has the potential to depart from U.S. tech stocks. I know that this idea often marks a local culmination of Bitcoin. The difference is that this time we see the potential for significant changes in capital flows, which will last.

Therefore, for a macro trader like me, Bitcoin feels the purest transaction here. You can't impose tariffs on Bitcoin, it doesn't care which boundary it is located, it provides high beta values for the portfolio without the current tail risks associated with US technology, I don't have to say anything about whether the EU can rectify its own affairs and provide pure exposure to global liquidity, not just US liquidity.

This market system is exactly why Bitcoin was born. Once the dust of deleveraging is settled, it will be the fastest horse, speeding up.

No comments yet